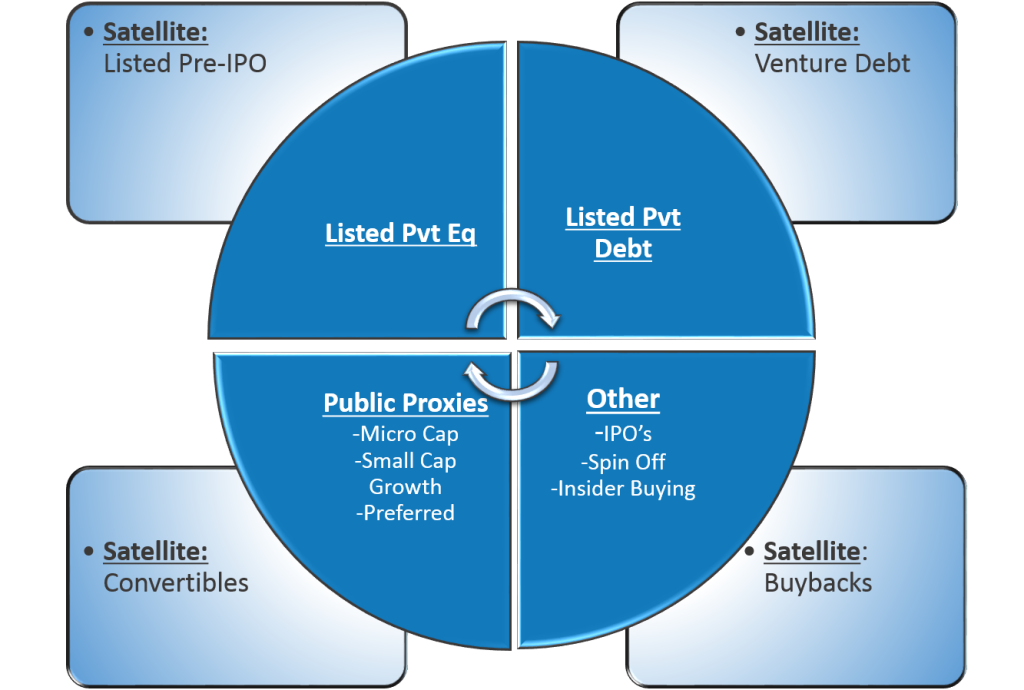

A Core and Satellite approach has been used to build this model, with the Core including low cost, primarily market capitalization weighted ETFs across four main segments of the market:

1 ) Listed private equity funds

2) Listed private debt funds

3) Publicly traded traditional proxies for private equity and

4) Publicly traded alternative proxies.

The Satellite allocations include ETFs that track alternative indices, attempting to add alpha over the Core indices. Examples include pre-IPO business development companies, venture debt, convertibles, companies doing buybacks, etc.